FinTech CRM selection is harder than most buyer guides admit. Standard CRM evaluation criteria — pipeline tracking, dashboards, email integration — barely scratch the surface of what FinTech operations actually need. The decision is shaped by KYC workflow design, AML case management, SOC 2 audit readiness, multi-state licensing complexity, and integration with the lending platform, payments processor, or trading system that holds your real business logic.

Generic CRM platforms can be configured to handle some of this. Few are designed for it. The gap shows up most painfully during audits and regulatory examinations — when the CRM that worked fine for sales tracking fails to produce the audit-ready compliance trail that examiners expect.

This guide walks through what FinTech operations leaders, compliance officers, and CTOs should evaluate when choosing CRM for a financial services business. It draws on FinTech deployments across lending platforms, payments processors, wealth management, InsurTech, NBFCs, and consumer finance — including the Series B FinTech case study where SuiteCRM was architected to pass SOC 2 Type II with zero findings.

If you’re at a FinTech company evaluating CRM options, this is the framework that surfaces the questions that actually matter.

TL;DR — FinTech CRM Buyer’s Quick Verdict

- The CRM is part of your compliance perimeter — it holds KYC, AML decisions, audit trail. Generic CRMs aren’t built for this.

- 7 decision criteria that actually matter: KYC workflow, AML case management, SOC 2 architecture, multi-state license tracking, core platform integration, AI explainability, 5-year TCO.

- Salesforce Financial Services Cloud lists $200/user/month + AI add-ons; per-user pricing breaks FinTech unit economics fast.

- SuiteCRM delivers comparable (often stronger) compliance posture at ~75% lower 5-year TCO, with SOC 2 Type II audit passes documented.

- Real outcome: Series B lender on SuiteCRM passed SOC 2 with zero findings, cut KYC time from 4.5 hrs → 90 min, saved ~$1.3M over 5 years vs Salesforce FSC.

- Implementation: 10–16 weeks for SOC 2-aligned mid-market deployments.

👉 Book a free FinTech CRM strategy call

Why FinTech CRM Selection Is Different

Three structural differences separate FinTech CRM requirements from CRM in other industries.

Difference 1: The CRM is part of the compliance perimeter. In most industries, the CRM holds customer information that’s incidentally regulated. In FinTech, the CRM holds customer information that’s centrally regulated — KYC data, beneficial ownership records, AML case decisions, sanctions screening results, and the audit trail of who made which compliance decisions when.

Regulators expect to see this data in the CRM (or an equivalent system), expect it to be accurate, and expect audit-ready documentation of how it got there. A CRM that’s not architected with this in mind creates compliance exposure rather than reducing it.

Difference 2: Multi-state regulatory complexity multiplies fast. A B2B SaaS company sells to customers in 50 states under one product. A FinTech company often holds licenses in dozens of states, each with their own renewal cycles, continuing education requirements, examination cycles, and operational rules. The CRM needs to track these license obligations and enforce state-specific workflow rules.

Most CRMs treat geography as a sorting field. FinTech needs geography to function as a regulatory boundary that actually changes workflow behavior.

Difference 3: The CRM doesn’t replace the core platform — it surrounds it. In most industries, the CRM is the system of record for customer relationships. In FinTech, the CRM lives alongside a core platform — a loan origination system, a payments processor, a trading platform, a policy administration system — that holds the actual business logic. The CRM handles everything around it: lead capture, KYC workflows, AML case management, customer service, marketing automation, retention.

This architectural reality means the integration pattern between CRM and core platform is often the highest-risk technical decision in the project. Get it wrong and the CRM either holds stale data (limiting usefulness) or creates duplicate state management (creating compliance and operational complexity).

For broader context, see our FinTech CRM solutions page and Finance CRM solutions.

The 7 Decision Criteria That Actually Matter

Surface-level CRM features look similar across vendors. The differences that determine whether a FinTech deployment succeeds or fails sit in the seven criteria below.

Criterion 1: KYC Workflow Architecture

KYC isn’t a feature you turn on. It’s a workflow that touches identity verification, beneficial ownership data capture, sanctions screening, PEP screening, adverse media checks, and documented decisioning. The CRM needs to orchestrate all of this with appropriate audit trails.

What to evaluate:

- Identity verification integration — most FinTech KYC uses Jumio, Onfido, Persona, Veriff, or Trulioo. Your CRM needs to integrate cleanly with whichever you’ve chosen.

- Beneficial ownership capture — small business and corporate KYC requires capturing up to 4-level ownership chains with each beneficial owner separately screened.

- Sanctions and PEP screening — typically ComplyAdvantage, Refinitiv (LSEG), Dow Jones, or Actimize. Real-time screening on initial KYC, periodic re-screening on existing customers.

- Decision documentation — every KYC decision needs documented reasoning, not just outcomes. Approved / declined / pending review with the specific factors that led to the decision.

- Audit trail — who reviewed, when, what they saw, what they decided. The compliance officer needs this on demand.

- Escalation workflow — complex cases need to route to senior reviewers with appropriate context preserved.

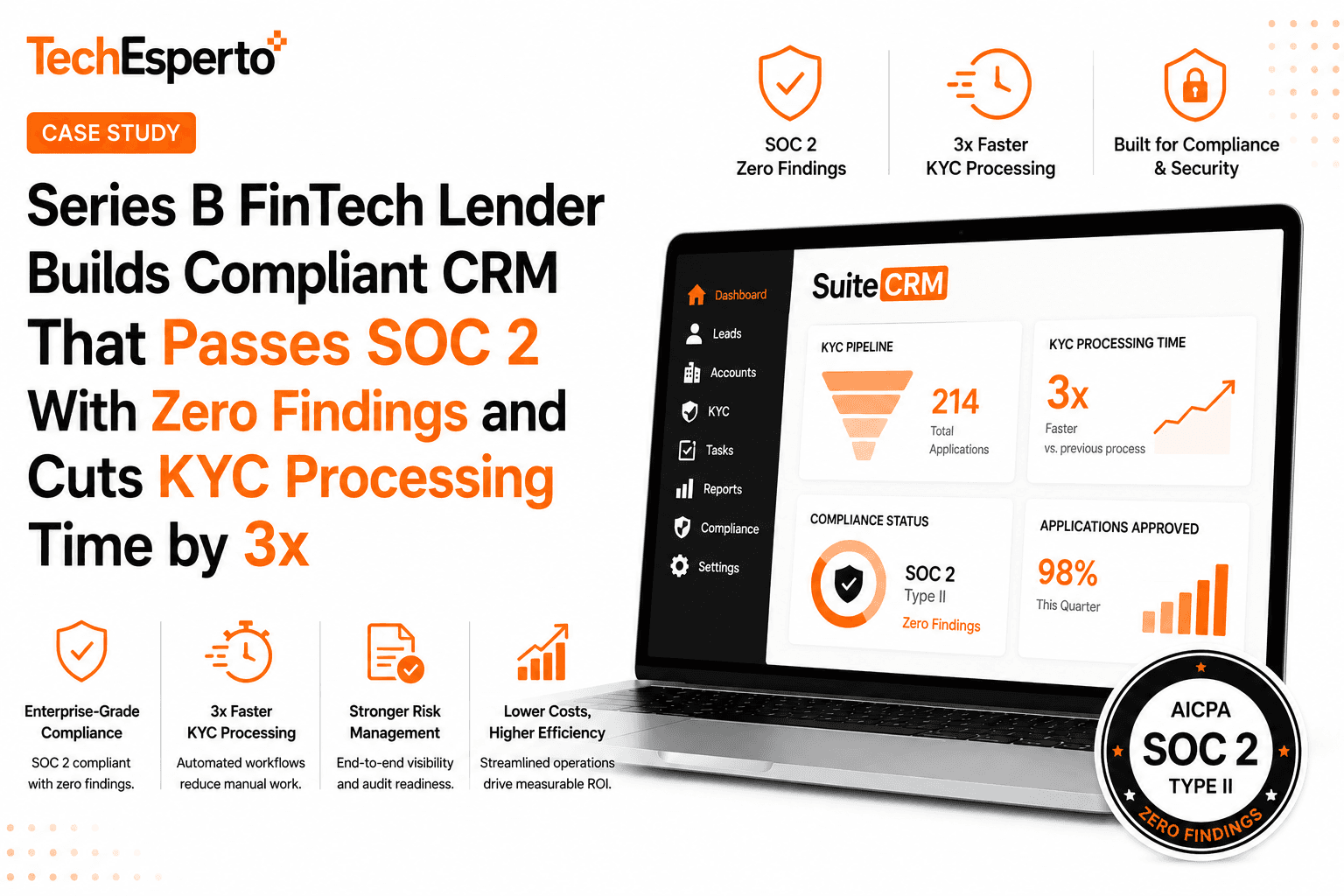

The KYC workflow in our Series B FinTech case study reduced processing time from 4.5 hours per application to under 90 minutes — a 3x throughput improvement driven by workflow design, not raw automation. See SuiteCRM Integration service for the broader integration approach.

Criterion 2: AML Case Management

When a transaction or pattern triggers an AML alert, what happens next determines whether your AML program survives an examination. Spreadsheets and email threads don’t pass audit. Centralized case management with documented workflow does.

What to evaluate:

- Alert intake from your AML provider with automatic case creation and assignment.

- Case lifecycle workflow — alert → investigation → decision → documentation → close, with timestamps at each transition.

- Standardized investigation templates — what evidence was reviewed, what decisions were made, what reasoning supported them.

- SLA tracking — alerts that age beyond defined thresholds escalate automatically.

- SAR (Suspicious Activity Report) preparation workflow — FinCEN-aligned data capture with appropriate narrative templates.

- Annual reporting automation — compliance team should be able to generate annual AML reporting in hours, not weeks.

- Audit-ready documentation — every case decision documented with reasoning, fully exportable for examiners.

The pattern that fails: ad-hoc case management in spreadsheets and email. The pattern that works: centralized case management with documented workflows and audit trails.

Criterion 3: SOC 2 Type II Architecture

SOC 2 isn’t a CRM feature. It’s an organizational compliance posture that the CRM either supports or undermines. Buyers underestimate how many CRM architectural decisions affect SOC 2 outcomes.

What to evaluate:

- Vendor agreements — the CRM vendor and any sub-processors need appropriate agreements covering data handling, breach notification, audit cooperation.

- Encryption at rest with customer-managed or auditable encryption keys.

- Encryption in transit with TLS 1.2+ enforcement.

- Audit logging at the application AND infrastructure level — who did what, when, from where.

- Access controls — role-based with regular access certification, plus session management. See our SuiteCRM Security Groups & Roles guide.

- Change management — every system change tracked, approved, logged.

- Incident response procedures — documented and practiced, not just written.

- Vendor management — sub-processor inventory with their own SOC 2 attestations where applicable.

- Backup and disaster recovery — encrypted, regularly tested, with documented RPO/RTO.

Our FinTech case study details a Series B lender whose SuiteCRM deployment passed first SOC 2 Type II audit post-implementation with zero CRM-related findings. The architectural work happens in Phase 1, not as retrofit.

For deeper compliance context, see CRM Data Security and Compliance, HIPAA + SuiteCRM technical setup (the same controls map to SOC 2), and GDPR + SuiteCRM setup for EU-facing fintech.

Criterion 4: Multi-State License and Regulatory Tracking

Most FinTech businesses operate across multiple state regulatory regimes. License management, continuing education requirements, examination cycles, and state-specific operational rules need to live somewhere the team actually maintains.

What to evaluate:

- License inventory by state, license type, license number, effective date, expiration date.

- Renewal workflow automation — 120 / 90 / 60 / 30-day reminders with multi-channel notifications.

- Continuing education tracking by individual and by license.

- State-specific operational rules — some states require specific disclosures, specific recording requirements, specific consumer protection workflows.

- Examination cycle tracking — when did the state last examine us, when is the next cycle expected.

- Document repository — license certificates, examination correspondence, regulatory correspondence.

The pattern that fails: a spreadsheet maintained by one person who’s increasingly overwhelmed as the state count grows. The pattern that works: license tracking integrated with workflow automation that proactively surfaces obligations before they become emergencies.

For our service approach to compliance-heavy implementations, see SuiteCRM Implementation service and Managed Support service.

Criterion 5: Core Platform Integration

The CRM-to-core-platform integration is the highest-risk technical decision in most FinTech CRM deployments. Done well, the CRM and core platform feel like one system. Done poorly, they create duplicate state management and reconciliation overhead that consumes operations team capacity.

What to evaluate:

- Specific core platform integration experience — has the vendor integrated with your lending platform / payments processor / trading platform before?

- Data flow architecture — what flows from CRM to core, what flows the other direction, where conflicts get resolved.

- Real-time vs. batch sync — depends on the use case; real-time has better UX but higher cost and complexity.

- Error handling — what happens when the core platform API fails or returns unexpected data.

- State reconciliation — how do CRM and core platform stay in agreement when both can update records.

- Compliance implications — which system holds the system-of-record version of customer data, who’s responsible for the compliance integrity of each.

The middleware approach we typically use isolates the CRM from core platform API quirks. See our CRM Integration Guide and SuiteCRM REST API Guide for the technical patterns.

Criterion 6: Customer-Facing AI With Compliance Awareness

Customer-facing AI in FinTech (chatbots, automated underwriting, AI-powered recommendations) comes with regulatory complexity that doesn’t exist in other industries. Decisions that affect credit access, insurance pricing, or financial product recommendations are subject to fair lending laws, disparate impact analysis, and increasingly specific AI governance frameworks.

What to evaluate:

- Explainability — every AI decision that affects a customer outcome needs documented reasoning. Black-box AI fails compliance review.

- Bias monitoring — fair lending analysis applies even when the decision is AI-assisted.

- Audit trails — what data did the model see, what version of the model, what was the output, who reviewed.

- Human-in-the-loop — high-stakes decisions need human review and override capability.

- Disclosure requirements — customers may need to be informed they’re interacting with AI in specific contexts.

For broader AI strategy in CRM, see our Complete Guide to AI for CRM and the AI for SuiteCRM service. For specific cost framework, see AI CRM Cost.

Criterion 7: Total Cost of Ownership That Doesn’t Eat Margin

FinTech businesses operate with specific unit economics. CRM cost that scales linearly with team headcount can quickly consume margin that should be funding growth.

What to evaluate:

- Per-user vs. flat pricing structure — Salesforce Financial Services Cloud lists at $200/user/month before any AI add-ons; per-user pricing scales with headcount whether or not new hires use it heavily.

- Compliance-related add-ons — Service Cloud, Einstein AI, additional CPQ licenses, integration platform fees often live in separate SKUs.

- Implementation cost — typically 50–150% of first-year licensing for enterprise platforms.

- Compliance architecture cost — SOC 2-aligned deployments add 20–30% to standard implementation cost regardless of platform; this isn’t optional.

- Ongoing compliance support — quarterly access certification, semi-annual control review, annual penetration testing all have cost components.

- 5-year TCO, not 1-year — most platforms look reasonable in year 1 and ugly by year 5.

The Salesforce Hidden Costs Calculator handles the TCO math for Salesforce comparisons. Our SuiteCRM Pricing Complete Guide covers the alternative cost structure.

FinTech CRM by Sub-Vertical

FinTech isn’t a single market — each sub-vertical has CRM requirements that shape the right configuration. Below are the patterns we’ve deployed across the most common ones.

CRM for Lending Platforms (Consumer + Commercial)

Lending operations need the CRM tightly integrated with the loan origination system (LOS) and the underwriting engine. Custom modules typically include Loan Application, KYC Check, Underwriting Decision, Servicing Note, and Collection Activity. Workflows automate document collection, KYC progression, underwriting routing, and collection escalation. The Series B case study above is a lending platform.

CRM for Payments Processors

Payments processors need CRM tightly integrated with the processing platform for merchant onboarding (KYC + KYB), risk monitoring, dispute handling, and merchant servicing. Custom modules: Merchant Application, KYB Documentation, Risk Score, Chargeback Case, Disbursement Schedule. Compliance focus: PCI-DSS posture, BSA/AML on transaction monitoring.

CRM for Wealth Management & RIAs

Wealth management firms need CRM tightly integrated with the portfolio management system. Custom modules: Client Profile (with risk tolerance + suitability), Account Aggregation, Meeting Notes (with regulatory recording), Annual Review. Compliance focus: SEC/FINRA recordkeeping, suitability documentation, communication archiving.

CRM for InsurTech

InsurTech needs CRM integrated with the policy administration system. Custom modules: Policy Application, Underwriting Decision, Claim, Producer Commission. State-by-state regulatory tracking. Compliance focus: state insurance regulator examinations, NAIC market conduct standards. See our broader Insurance CRM solutions.

CRM for Consumer Finance

Consumer finance (credit cards, BNPL, personal loans, deposit products) needs CRM at high volume with low per-customer cost — making per-seat SaaS CRM economics particularly brutal. Custom modules: Account, Servicing Case, Collections Activity, Dispute. Compliance focus: TCPA on outbound calling, FDCPA on collections, CFPB consumer protection.

CRM for NBFC / Indian FinTech

Non-banking financial companies in India face RBI compliance, KYC under PMLA, and state-by-state operational requirements. Custom modules: Loan Application with Aadhaar / PAN integration, KYC Documentation, Underwriting, Collection, RBI Reporting. The combination of SuiteCRM’s customization depth + zero per-seat license + self-hosting on Indian cloud (AWS Mumbai / Hyderabad) makes it the dominant fit for Indian fintech.

CRM for Crypto / Digital Asset Firms

Crypto-native firms need CRM integrated with on-chain analytics and KYT (Know Your Transaction) providers like Chainalysis, TRM Labs, or Elliptic. Custom modules: Wallet Profile, Transaction Risk Score, Travel Rule Compliance Record, Sanctions Match. Compliance focus: FinCEN MSB registration, state money transmitter licenses, OFAC sanctions screening, BSA/AML.

The patterns above are the most common. Anything FinTech-adjacent (PayTech, RegTech, embedded finance, neobanks) follows variations on these themes.

Why Off-the-Shelf Salesforce Financial Services Cloud Often Underperforms

Salesforce Financial Services Cloud is the default enterprise option for FinTech CRM. It works well for some organizations — typically large established financial institutions with internal Salesforce competence and budget tolerance for high licensing costs.

For most growth-stage FinTech companies (Series A through Series C, 30–300 person operations), FSC underperforms its alternatives for four reasons.

Reason 1: Per-user pricing breaks unit economics. FSC lists at $200/user/month base, plus add-ons. For a 100-person FinTech operation, that’s $240,000/year in licensing alone, before Einstein AI ($30K+), Service Cloud licenses for support teams ($20K+), and integration platform fees. As FinTech teams scale into operations roles (compliance, customer service, fraud, collections), per-user costs compound disproportionately to revenue.

Reason 2: KYC and AML workflow customization is expensive on Salesforce. Specific KYC and AML workflows often need real customization — beneficial ownership data capture beyond out-of-box, AML case management beyond Salesforce’s default, multi-state regulatory variations. On Salesforce, every meaningful customization either requires APEX development (expensive) or runs into platform limits.

Reason 3: Vendor lock-in compounds during regulatory examinations. Once a FinTech is deeply customized on FSC, switching costs become prohibitive. Salesforce knows this and prices accordingly. The 8% annual list price increases that look reasonable in year 1 become budget-breaking by year 5. For broader analysis, see our Salesforce Hidden Costs breakdown.

Reason 4: Open architectures support audit better. Counterintuitively, open-source CRM with documented architecture often passes SOC 2 and regulatory audits more cleanly than proprietary platforms. Auditors can review architecture documentation directly rather than relying on vendor attestations. The transparency works in your favor during examinations.

For broader comparison context, see SuiteCRM vs Salesforce and Salesforce Renewal Decision framework.

What Good FinTech CRM Looks Like in Practice

The Series B FinTech case study covers what good FinTech CRM looks like operationally. Quick summary of outcomes from a lending platform, 14 months post-launch:

- SOC 2 Type II audit passed with zero CRM-related findings

- KYC processing 3x faster — from 4.5 hours per application to under 90 minutes

- AML case management consolidated from scattered spreadsheets to centralized workflow with full audit trail

- Multi-state license tracking automated — zero license renewal misses in 14 months (after two near-misses in the prior 18 months)

- Compliance officer time recovered: approximately 12 hours per week previously spent on manual case management and reporting

- Loan officer productivity: 35% improvement in applications processed per week

Implementation cost: $55,000 plus $5,500/month ongoing managed services. Compared to Salesforce FSC’s projected 5-year TCO of ~$1.7M, the SuiteCRM deployment lands at approximately $390K over 5 years — saving approximately $1.3M while delivering compliance posture stronger than the alternative.

Full architecture and outcome detail in the FinTech CRM case study.

5-Year TCO: FinTech CRM Cost Comparison

For a 100-user FinTech operation with KYC + AML + multi-state licensing requirements:

| Cost line (5 years) | Salesforce FSC + add-ons | SuiteCRM with TechEsperto |

|---|---|---|

| Year 1 license + AI add-ons | $270K | $0 |

| Year 2–5 license (with ~8% escalation) | $1.25M | $0 |

| Implementation (compliance-aligned) | $150K | $80K |

| Compliance architecture + audit support | $50K | $40K |

| Ongoing managed services / Premier Support | $100K | $300K (flat managed, 5 yrs) |

| 5-Year Total | ~$1.82M | ~$420K |

SuiteCRM savings at 100 users: ~$1.4M over 5 years.

Run your specific scenario in the Salesforce hidden cost calculator. For the board-level financial framing, see SuiteCRM for CFOs.

Vendor Evaluation Checklist

When evaluating FinTech CRM vendors, ask each candidate the same questions and compare responses. The questions below surface differences that surface-level demos hide.

Compliance and architecture:

- Will you sign appropriate vendor agreements for our regulatory framework?

- What’s your encryption posture at rest and in transit, and who controls the keys?

- What audit logging is captured, at what depth, with what retention?

- Have you delivered SOC 2 Type II audits with zero findings for FinTech clients?

- What sub-processors have access to our data and do they have their own attestations?

KYC and AML workflows:

- Which specific identity verification, sanctions screening, and AML providers have you integrated with?

- What does your KYC workflow look like end-to-end for a small business with multiple beneficial owners?

- How does AML case management work — alert intake, investigation workflow, documentation, SAR preparation?

- Can your platform produce audit-ready reports on demand?

Multi-state and regulatory:

- How do you handle multi-state license tracking with state-specific renewal cycles and CE requirements?

- Can workflow rules vary by state for state-specific operational requirements?

- How is regulatory correspondence and examination response tracked?

Core platform integration:

- Which specific lending platforms / payments processors / trading platforms have you integrated with previously?

- What’s your integration architecture (direct API, middleware, ETL)?

- How does the integration handle core platform API failures?

Total cost of ownership:

- What’s the year 1 cost broken down into licensing, implementation, ongoing support, infrastructure, and compliance architecture?

- What’s the year 5 cost projection assuming our team grows by X%?

- What add-ons or modules typically become required as we scale?

- What are the annual price escalation clauses?

For broader vendor evaluation framework, see How to Choose a SuiteCRM Partner and Ultimate CRM Buying Guide.

Getting Started

If you’re evaluating FinTech CRM options, three steps in order:

Step 1: Get clarity on your compliance posture. Document current state — what compliance frameworks apply, where current gaps exist, what your audit timeline looks like. The free SuiteCRM Implementation Checklist provides a structured audit framework.

Step 2: Quantify the cost of alternatives. Most FinTech companies underestimate the cost of staying on enterprise CRM platforms. The free Salesforce Hidden Costs Calculator automates the TCO math for Salesforce Financial Services Cloud comparisons.

Step 3: Get a candid second opinion. Book a free 30-minute strategy call — we’ll walk through your specific compliance requirements, core platform integration needs, and budget framework, and give you an honest recommendation. No pitch, no commitment.

For deeper context, see our FinTech CRM solutions, the FinTech case study, Finance CRM solutions, Insurance CRM solutions, and broader CRM strategy content including Build vs Buy CRM and Pricing.

Frequently Asked Questions

What is FinTech CRM?

FinTech CRM is customer relationship management software architected for financial services businesses — lenders, payments processors, wealth managers, InsurTech, NBFCs, neobanks. Unlike generic CRM, FinTech CRM treats KYC, AML case management, multi-state licensing, SOC 2 audit posture, and integration with the core platform (LOS, payments processor, trading system) as first-class requirements rather than add-ons.

What’s the best CRM for FinTech in 2026?

For most growth-stage FinTech operations (Series A through Series C), SuiteCRM delivers the best balance of compliance capability, customization depth, and total cost of ownership. Salesforce Financial Services Cloud is the default enterprise option but per-user pricing increasingly breaks FinTech unit economics. See the comparison sections above for the deeper analysis.

What’s the best CRM for a lending platform specifically?

A CRM tightly integrated with your loan origination system, with custom modules for Loan Application + KYC + Underwriting + Servicing + Collections. SuiteCRM is the most common deployment pattern for growth-stage lenders because the custom-module architecture handles lending-specific workflows without per-seat license cost. See our Series B lending case study.

What’s the smallest FinTech operation that should invest in a real CRM?

Roughly 8+ people across sales, compliance, and operations, plus regulatory complexity that exceeds what spreadsheets can manage. Pre-revenue or pre-licensing FinTech can often operate on basic tools. Once you have KYC obligations, AML workflows, and multi-state operations, the operational complexity creates CRM value capture.

Do we need a dedicated CRM if we already have a lending platform / payments processor / trading system?

Yes, for most FinTech operations above the smallest scale. Core platforms handle the financial transactions and product logic well. They handle customer acquisition, KYC orchestration, compliance case management, multi-state licensing, customer service, marketing automation, and retention workflows poorly or not at all. The CRM-core-platform pairing is the dominant pattern across FinTech for good reason.

How do we handle the SOC 2 risk of adding another system to our stack?

By architecting the CRM as part of the SOC 2 perimeter from Phase 1, not retrofitting after. Done correctly, a SOC 2-aligned CRM strengthens your compliance posture rather than weakening it — because it formalizes workflows that were previously informal (and therefore unauditable). The FinTech case study details a deployment that passed SOC 2 Type II with zero CRM-related findings.

What’s the realistic timeline for a FinTech CRM implementation?

Typically 10–16 weeks for SOC 2-aligned mid-market deployments. Faster than that usually means compliance corners were cut. Longer than that usually means scope was too broad or vendor isn’t efficient. The FinTech case study ran 12 weeks from kickoff through go-live.

Can the CRM replace our lending platform / payments processor?

No, and any vendor suggesting otherwise should be evaluated skeptically. Core platforms handle regulated financial transactions with specific compliance requirements; CRMs handle relationship management and operational workflows. They work alongside each other, not as replacements.

What about specific compliance frameworks beyond SOC 2?

Most FinTech compliance frameworks (PCI-DSS for payments, state-specific lending licenses, OFAC sanctions compliance, Bank Secrecy Act for AML, GLBA for privacy) can be architected into the CRM with appropriate planning. Some specialized frameworks (FedRAMP for federal contracts, specific state-level financial services frameworks) require additional architectural work. Phase 1 discovery scopes what’s required for your specific situation.

How does FinTech CRM differ from generic CRM?

Generic CRM treats customer data as a sales asset. FinTech CRM treats customer data as a regulated asset — every record subject to KYC, AML, sanctions screening, audit logging, retention policies, and disclosure requirements. The architectural decisions (encryption, hosting, access control, audit trail, integration) are fundamentally different. Generic CRM configured for FinTech usually fails its first regulatory examination.

Will the CRM integrate with our specific core platform?

In almost all cases, yes. We’ve integrated with custom-built lending platforms, third-party LOS systems, major payments processors, trading platforms, and policy administration systems. Each has specific patterns; Phase 1 includes integration scoping for your specific situation. See our SuiteCRM Integration service for the technical approach.

What if we’re already on Salesforce FSC and considering alternatives?

You’re in the same position as the case study buyer — running per-user licensing that doesn’t scale with FinTech unit economics, with customization costs that compound. The Salesforce FSC migration path is similar to the standard Salesforce → SuiteCRM migration. See Salesforce → SuiteCRM Migration service, Salesforce Renewal Decision framework, and the Migrate Salesforce to SuiteCRM Guide for the methodology.

Does SuiteCRM work for NBFC / Indian fintech specifically?

Yes — and it’s increasingly the dominant choice. SuiteCRM’s customization depth handles RBI-specific workflows (Aadhaar / PAN integration, RBI reporting templates, state-by-state operational rules), zero per-seat license matches Indian fintech unit economics, and self-hosting on AWS Mumbai / Hyderabad keeps data residency clean. See our FinTech CRM industry page for the deeper sub-vertical breakdown.

Can AI features be added to FinTech CRM under fair-lending rules?

Yes — with explainability + bias monitoring + human-in-the-loop on high-stakes decisions. We deploy AI use cases (lead scoring, churn prediction, document classification) on top of SuiteCRM using OpenAI / Anthropic / private open-weights models with full audit trails. For high-stakes decisions affecting credit access, human-in-the-loop is mandatory regardless of model. See our AI for CRM 2026 guide.

What’s the difference between FinTech CRM and Insurance CRM?

Significant overlap (KYC, audit posture, multi-state licensing, integration with a core platform). InsurTech adds: policy lifecycle management, claims workflow, producer commission, state-specific filings. See our dedicated Insurance CRM solutions page for the InsurTech-specific differences.

How do we get started?

Best starting point is the free 30-minute strategy call. We’ll walk through your compliance posture, KYC/AML requirements, core platform integration needs, multi-state operations, and budget framework — and give you a candid recommendation. No pitch, no commitment.

Ready to Stop Letting Your CRM Eat Your Margin?

For most growth-stage FinTech operations, the CRM decision quietly compounds into one of the largest line items on the P&L by year 3. Getting it right early — choosing a platform that scales with your team, supports your compliance posture, and integrates cleanly with your core platform — is one of the highest-leverage operational decisions a CFO or COO will make.

👉 Book a free FinTech CRM strategy call — written recommendation in 5 business days covering compliance posture, integration approach, fixed-fee build quote, and 5-year TCO comparison.

👉 Calculate your 5-year CRM TCO — works for Salesforce FSC, HubSpot, Pipedrive, and other per-seat platforms.

👉 Read the FinTech CRM case study — SOC 2 Type II passed with zero findings, ~$1.3M saved over 5 years vs Salesforce FSC.

Also Read

SuiteCRM Security Groups & Roles Guide